Some restaurant claims stay small.

Some do not.

Umbrella or Excess Liability insurance exists for the claims that get bigger than expected.

And if you own a restaurant, “bigger than expected” is not exactly a foreign concept. You have seen a quiet Tuesday turn into a full dining room with two call-offs and one printer having a spiritual crisis.

Insurance can feel the same way.

What Umbrella or Excess Liability does

An Umbrella or Excess Liability policy may provide additional liability limits over certain underlying policies.

That means it can sit above policies like:

- General Liability

- Business Auto

- Employers Liability

- Liquor Liability, depending on the policy

- other scheduled underlying policies

The details matter. Not every umbrella sits over every line.

That is why you need to check what it actually follows.

Why restaurants may need higher limits

Restaurants can face claims involving:

- customer injuries

- serious slip and fall incidents

- food-related allegations

- auto accidents

- liquor-related incidents

- property damage

- employee injury-related employer liability issues

A basic liability limit may be enough for some smaller claims. But bigger claims can push limits quickly.

Umbrella coverage gives the business another layer of protection when eligible underlying limits are exhausted.

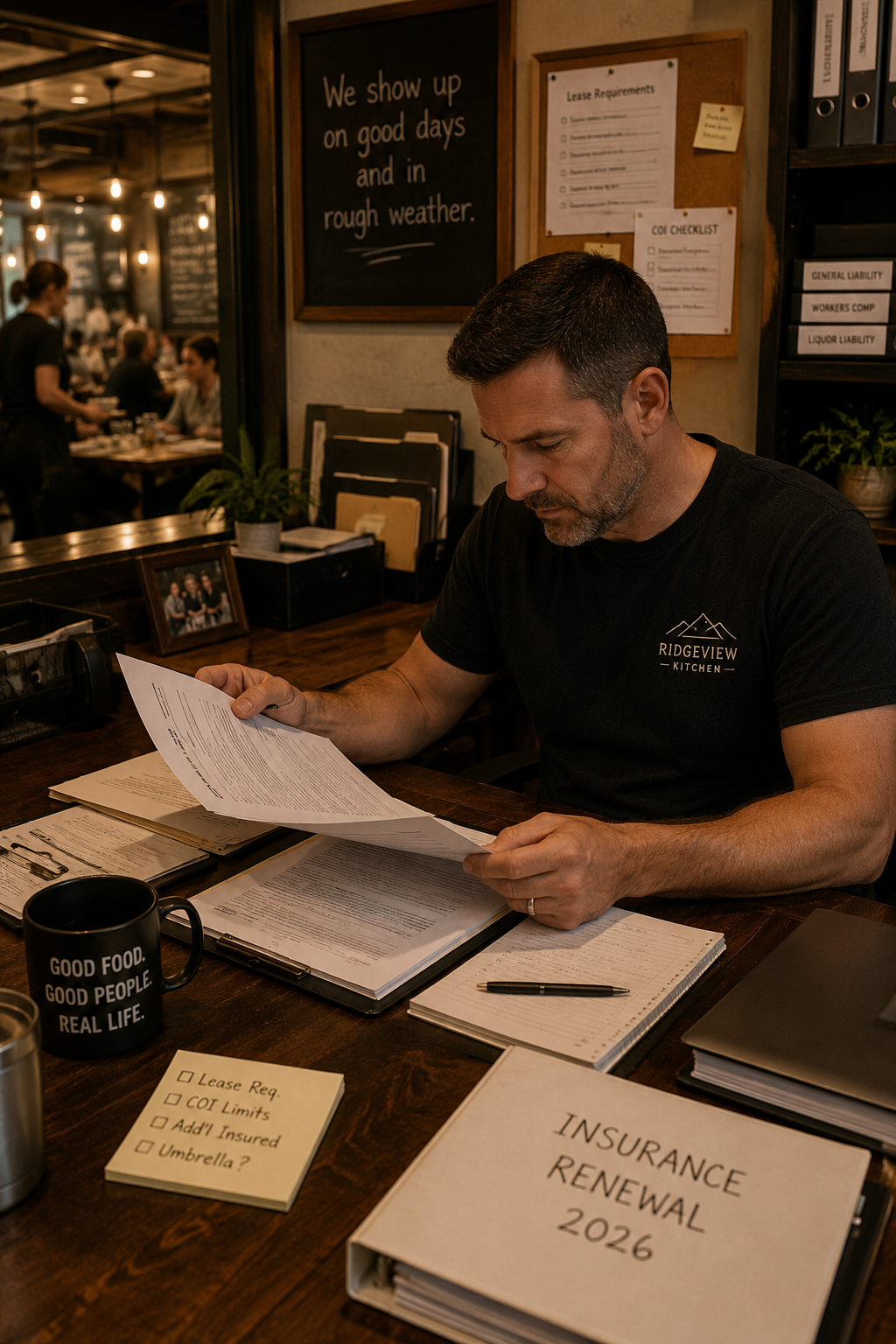

Lease and contract requirements

Sometimes the umbrella conversation starts because of a lease.

Landlords may require higher liability limits. So may lenders, event venues, vendors, municipalities, or contract partners.

If your lease or contract requires a certain limit, do not assume your current policy meets it.

Ask:

- What limits are required?

- Does the umbrella apply over the required coverage?

- Does the certificate show the right limits?

- Are additional insured requirements included?

- Are there exclusions that matter?

Certificates are not decorations. They are proof. They need to match the actual coverage setup.

Umbrella is not a fix for everything

An umbrella is not a magic dumpster you throw all uncovered claims into.

It usually follows the underlying policy terms. If something is excluded underneath, the umbrella may not solve it.

That is why umbrella coverage should be reviewed alongside the underlying policies.

Think of it like adding more pans to the line. Helpful, yes. But if the station itself is wrong, more pans do not fix the service.

What restaurant owners should review

Ask:

- Do we have an umbrella or excess policy?

- What limit applies?

- What underlying policies does it sit over?

- Does it include liquor liability?

- Does it include auto?

- Does it satisfy lease or contract requirements?

- Are there gaps between underlying limits and umbrella requirements?

This is especially important for restaurants with alcohol, delivery, catering, event exposure, or high customer traffic.

Want an umbrella coverage gut check?

If your restaurant has a lease, alcohol exposure, delivery, catering, or higher customer traffic, umbrella coverage deserves a review.

Send your declarations page and any landlord or contract requirements.

We will help you understand what looks solid and what deserves a second look.

Send your dec page to:

INeedHelp@Silver-LiningIns.com